Thinking about a waterfront condo in Bal Harbour but unsure how to read the market? You are not alone. Bal Harbour is small, exclusive, and shaped by a handful of high-end buildings, which can make prices and days on market feel unpredictable. In this guide, you will learn how inventory tiers work, what truly drives value, how seasonality influences timing, and how building fees and rules affect your bottom line. Let’s dive in.

Bal Harbour at a glance

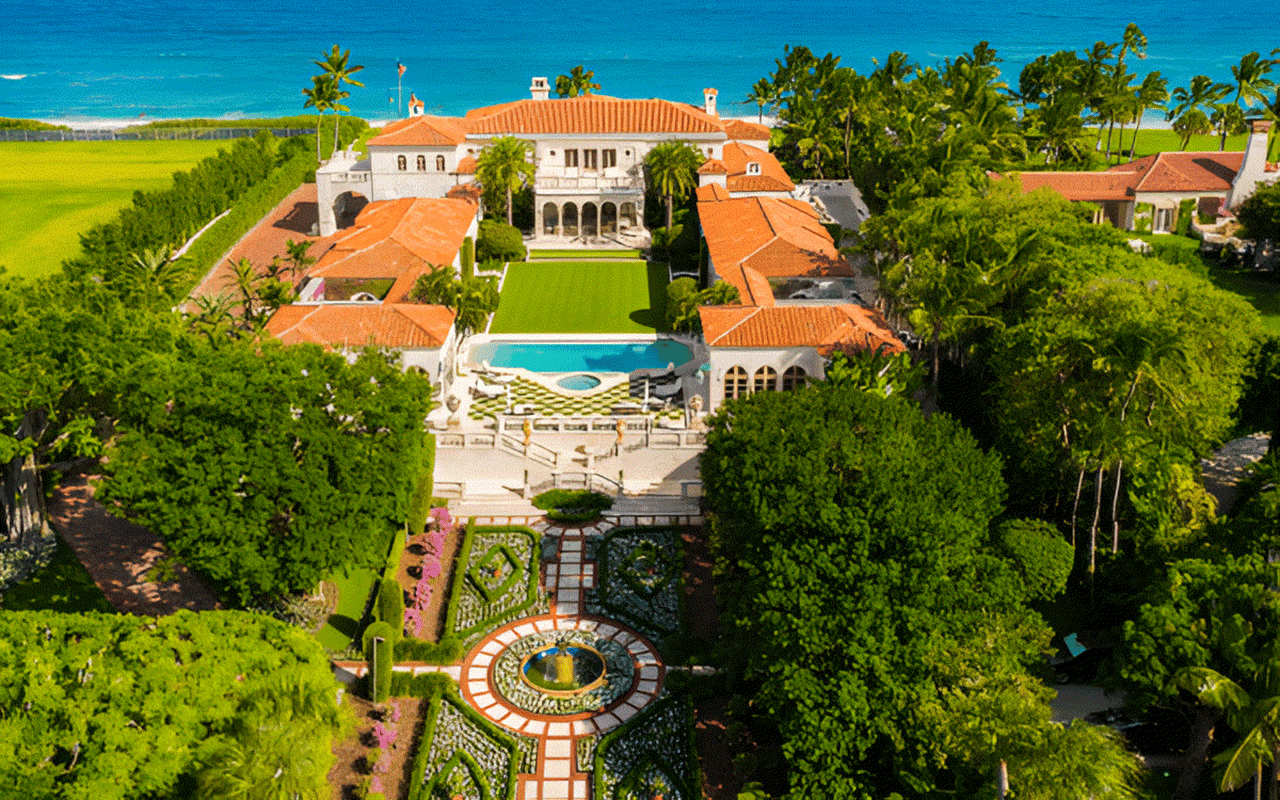

Bal Harbour is a compact, luxury beachfront village in Miami-Dade County with limited land and a small number of waterfront buildings. Most properties are full-service mid to high-rise condos rather than single-family waterfront homes. Because supply is tight and turnover is low, a few large closings can move headline averages in any given year.

In a market this narrow, context matters. Median price swings can look dramatic when a penthouse or trophy unit closes. To get a clearer picture, focus on price per square foot and closed sales volume rather than one-off headline sales.

Bal Harbour inventory tiers

Bal Harbour functions on three practical tiers. Understanding which tier fits your goals will help you compare options and value correctly.

- Entry waterfront tier: Smaller 1 to 2 bedroom units or older, less renovated homes with water or beach access. These may sit on lower floors or have partial views. They appeal to seasonal users and investors who value location over designer finishes.

- Mid tier: Renovated 2 to 3 bedroom units on middle to higher floors with stronger amenities and better view lines. These tend to attract full-time owners and higher-end investors.

- Upper and trophy tier: Large, often full-floor or penthouse residences with bespoke finishes, private elevators, full ocean frontage, and unobstructed views. This segment is distinct, with longer marketing timelines and a high share of cash buyers.

New construction inside the village limits is rare, so resale dynamics set the tone. Renovated units usually move faster, while dated inventory can linger until priced to reflect renovation needs.

What drives value

Several factors influence pricing in Bal Harbour. Rank your must-haves early so you can move quickly when the right home appears.

- View line and orientation: Direct, unobstructed ocean exposure commands the strongest premium. Partial ocean or bay views follow, then city or interior views.

- Floor level: Higher floors are prized for views and privacy. Lower floors can be discounted if exposure is blocked or street noise is a factor.

- Building quality and services: Full-service buildings with 24-hour security, valet, private beach services, and robust amenities trade at a premium over limited-service buildings.

- Renovation level: Turnkey, designer-finished units sell faster and closer to ask. Original or dated units need a renovation budget and carry a discount.

- Parking and storage: Deeded spaces, multiple spots, and private storage add real-world convenience and value.

- Association financial health: Strong reserves and no pending assessments support pricing. Active litigation, weak reserves, or large special assessments suppress buyer demand.

- Resilience and insurance: Impact glass, upgraded infrastructure, and favorable flood elevation can reduce perceived risk and support value.

- Rental rules and occupancy: Flexible rental policies can help investors. Full-time owners sometimes prefer buildings with more owner-occupancy and tighter rental rules.

Financing and carrying costs

Cash remains common at the high end, but many buyers still use jumbo financing. Lenders will review association documents, reserve studies, owner-occupancy levels, and any special assessments. That means a building’s financials can affect not only value, but also the pool of buyers who can close.

In addition to the purchase price, model your true monthly and annual costs. Property taxes in Miami-Dade and homestead eligibility only apply to primary residences. Add HOA fees and insurance obligations to get the full picture. Luxury waterfront buildings often have higher monthly fees due to staffing, amenities, insurance premiums, and reserve funding.

Seasonality and timing

South Florida’s peak season typically runs November through April. That is when seasonal buyers are most active and well-priced listings can see strong interest. Spring is a common closing window for sellers who list in late fall.

From summer through early fall, you may face fewer competing buyers. That can help with negotiation, especially if a seller is motivated. If you plan inspections or closings during hurricane season, build in time for insurance coordination and any lender requirements.

For sellers aiming for top pricing, positioning your listing to capture winter buyers can be advantageous. Presentation, professional photos, and accurate pricing aligned to the right tier matter more than ever.

Building types and fees

Most Bal Harbour waterfront options are condo towers, and not all buildings are equal in services or cost structure. Here is how the main types compare.

- Trophy high-rise luxury towers: Highest per square foot pricing, large amenity packages, and extensive staffing. HOA fees tend to be the highest due to services and insurance needs.

- Boutique or older waterfront buildings: Fewer units, more modest services, and sometimes lower fees. Watch for deferred maintenance or upcoming projects that could result in special assessments.

- Low-rise waterfront complexes: Smaller footprints near beach access. These often attract buyers who value privacy over a large amenity suite.

When comparing buildings, evaluate the amenity-to-fee balance. High fees can make sense if they include beach services, valet, robust security, and well-funded reserves. Beyond a point, however, elevated fees can narrow the buyer pool, especially for financed buyers and investors.

What HOA fees include

Not all fees cover the same items. Review the fine print so you do not compare apples to oranges.

- Staffing and services: Concierge, security, valet, and maintenance

- Common area operations: Pools, landscaping, beach services, utilities in common areas

- Building insurance: Wind and flood coverage under the master policy

- Reserves and capital projects: Funding for repairs and future work

Ask what is included versus separate. Some buildings include cable, internet, or water. Others bill these items directly to the owner.

Buyer due diligence checklist

If you are early in the process, start with a focused list. The goal is to confirm building health and true carrying costs before you fall in love with a view.

- Association documents: Budget, reserve study, monthly HOA, year-to-date financials, and the last 12 months of meeting minutes

- Capital projects: Any pending or recently completed work and associated special assessments

- Insurance: Master policy coverage and what the owner must carry, including flood and contents

- Structural status: Recertification milestones, inspection results, and any planned remediation

- Rental policy: Minimum lease terms, rental caps, and current occupancy mix

- Parking and storage: Deeded versus assigned spaces and availability of lockers

- Litigation: Any open or recent lawsuits involving the association

- Utilities and extras: What the fee includes and what is billed separately

- Title items: Deed type, encumbrances, or restrictions tied to the unit

Seller prep checklist

Bal Harbour buyers expect a polished, turnkey experience. Set the stage so your listing rises above the competition.

- Documentation: Prepare an estoppel, current budget, reserve study, recent minutes, and a summary of insurance

- Presentation: Address obvious maintenance or cosmetic items. Staging and high-quality photography should highlight view lines and amenities

- Pricing: Align to the correct tier and account for view, floor, finishes, and association health

- Timing: Target winter buyers when possible. If listing off-season, plan for longer market time and strategic price reviews

- Financing awareness: Understand condo eligibility requirements so you can help qualified buyers close smoothly

Insurance, resilience, and flood exposure

Wind and flood insurance costs have become a bigger factor across coastal Florida. Review the building’s master policy and ask what it covers versus owner obligations. Buildings with impact glass, newer systems, and favorable elevations may be viewed as less risky by buyers.

Also confirm flood zone designation and any mitigation steps the association has taken. Insurance costs can change the math on affordability, especially in buildings with large common areas or complex amenity packages.

Reading the data in a small market

In Bal Harbour, sample sizes are small. That means one large closing can skew median prices. To keep perspective, track price per square foot across comparable buildings and watch closed sales volume. Give more weight to renovated units in similar tiers and floor ranges with comparable view lines.

When you evaluate comps, focus on supply within your submarket. For example, a renovated 2 bedroom on a high floor with direct ocean views belongs in a different comparison set than a lower-floor unit with partial views or dated finishes.

Marketing notes for trophy and upper tiers

Trophy residences often attract seasonal and international buyers. Virtual tours, building-level storytelling, and concierge coordination can be essential. Given low turnover, broker networks sometimes place units before they go public. If you plan to sell in the trophy tier, expect a longer timeline and value-driven buyers who scrutinize association health and fees.

When to move forward

If you find a unit that checks your view line, floor, finish level, and association criteria, move decisively. The best-situated homes can draw multiple offers, especially in season. At the same time, patience can pay off in the off-season when motivated sellers are open to negotiation.

If you are selling, invest in presentation. In a market where buyers pay premiums for views and turn-key finishes, the right preparation helps you protect pricing and compress time on market.

How a concierge approach helps

Bal Harbour buyers and sellers often juggle travel, family, and business schedules. A hospitality-style process keeps things smooth. Expect coordinated showings, clear timelines, and proactive document gathering from the association so you can make confident decisions quickly. The details around reserves, insurance, and structural status can be the difference between a stress-free closing and a costly surprise.

Ready to navigate Bal Harbour with clarity and confidence? Schedule a private waterfront consultation with Marine Rollins to map your tier, timing, and next steps.

FAQs

What makes Bal Harbour condo prices move most?

- View line, floor level, building services, renovation quality, and association health have the biggest impact on value.

How do HOA fees affect affordability in Bal Harbour?

- Fees fund staffing, amenities, insurance, and reserves, so higher-fee buildings can offer more services but also raise your carrying costs.

When is the best season to buy or sell in Bal Harbour?

- Peak demand runs November through April, while summer to early fall can offer less competition and more room to negotiate.

What condo documents should I review before buying?

- Ask for the budget, reserve study, HOA amount, recent minutes, insurance summary, any assessments, and recertification or inspection updates.

How do lenders evaluate Bal Harbour condos?

- Lenders review association reserves, owner-occupancy levels, assessments, and litigation, which can affect loan approval and terms.

What risks should I consider near the water?

- Review wind and flood insurance, flood zone designation, building resilience features, and any upcoming structural work or recertification milestones.