Buying on Indian Creek Island is unlike any other Miami real estate experience. Inventory is tiny, showings are tightly controlled, and many sales never hit the public market. If you value privacy, speed, and precision, you need a clear plan and a discreet team that can move fast. In this guide, you’ll learn how the island works, how to get in the door, what to prepare before you write an offer, and the exact due diligence that protects you. Let’s dive in.

Know the market you are entering

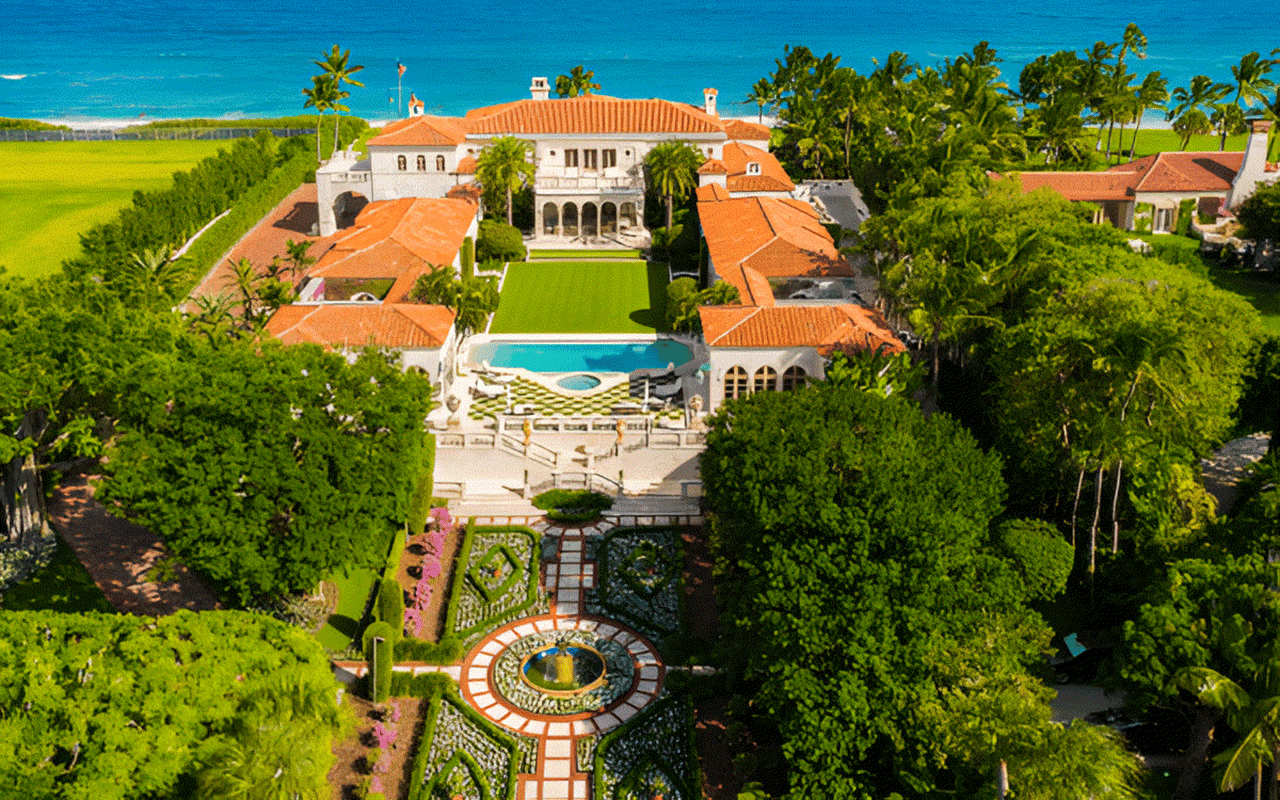

Indian Creek, officially the Village of Indian Creek, is an ultra‑private, gated island in Biscayne Bay with very large waterfront parcels and a small, highly affluent residential base. Sales are rare and often handled off‑market through trusted broker networks and direct introductions. Public MLS comparables can be limited or irrelevant because estates are bespoke, and recent private trades carry the most weight.

What this means for you: treat the search like a concierge process. Confidentiality, timing, and certainty of close often matter more than open bidding. Expect to verify your capacity before you receive details and before you step onto the island for a showing.

Build your acquisition team early

Your goal is to remove friction and show sellers you are ready. Engage these specialists as soon as you start the search:

- Lead luxury broker with Indian Creek experience and off‑market access.

- Florida real estate attorney who understands coastal permits and entity structuring.

- Title company that routinely handles high‑value Florida island closings.

- Lender with jumbo and coastal lending expertise if you are not all‑cash.

- Insurance broker for high‑value coastal properties to model wind and flood premiums.

- Surveyor and marine engineer to evaluate boundaries, seawalls, and docks.

- General inspector with specialists for roof, HVAC, electrical, mold, and IAQ.

- CPA and estate counsel for privacy, tax, and cross‑border planning if needed.

Plan access and showing protocols

Indian Creek is gated with controlled entry. Showings, inspections, and contractor visits must be scheduled in advance and cleared with island security. Sellers often require NDAs and restrict photography or recording. Your broker coordinates guest lists, confirms IDs, and sets rules of engagement so your visit is smooth and discreet.

Pro tip: have signed NDAs and a no‑media policy ready before walkthroughs. Pre‑clear any third‑party professionals so they are not turned away at the gate.

Prove readiness before you tour

On the island, readiness opens doors. Listing brokers commonly request immediate proof of funds before sharing full property details or granting access. Bank statements or a banker’s letter that documents liquid capacity is standard. For very high price points, be prepared for source‑of‑funds verification to satisfy compliance.

If you plan to finance, start lender conversations early. Jumbo lenders underwriting large coastal properties order specialized appraisals and review wind, hurricane, and flood exposure. Early pre‑approval saves time when you find the right home.

Choose your ownership structure

Many buyers use LLCs or trusts for privacy, liability, and estate planning. These structures affect title, insurance binders, lender documentation, and closing signatures. Set your entity up before you write an offer so you can move quickly and avoid re‑papering later. Ask counsel to review potential homestead implications, bank KYC, and tax reporting if you are a cross‑border buyer.

Source properties through private channels

Most opportunities circulate through trusted broker relationships, private owner outreach, and referrals from family offices or advisors. Expect to sign NDAs and share buyer credentials so sellers feel comfortable engaging. Your broker’s network, reputation, and precision with confidentiality are key advantages.

Structure an offer that wins

Sellers often value discretion, speed, and certainty. Cash offers with minimal contingencies can be powerful. If you include contingencies, keep them focused and timely, such as title, survey, inspection, and financing if applicable. Consider stronger earnest money and shorter windows for diligence when the asset is competitive.

Wire security is essential. Confirm escrow instructions by phone directly with the title or closing agent you already know. Large transactions are targets for fraud, so never rely on last‑minute emailed changes.

Run waterfront‑specific due diligence

Waterfront estates require deeper checks than a typical home. During your inspection window, prioritize these items:

- Title search and title insurance. Confirm ownership, easements, dock rights, and any covenants or restrictions. Review historical permits for structures and shoreline work.

- Boundary and marine survey. Verify lot lines, bulkhead location, seawall alignment, and dock configuration. Waterfront boundaries and mean high water lines are material.

- Whole‑home inspection. Evaluate structure, roof, electrical, plumbing, HVAC, and hurricane mitigation features. Look for documented wind upgrades that can reduce insurance costs.

- Marine structural assessment. Inspect seawalls, pilings, and fendering, and confirm navigable channel access. Repair exposure here can be significant and affects insurability and use.

- Environmental and regulatory review. Shoreline work, docks, dredging, or lifts often require permits from the U.S. Army Corps of Engineers and the Florida Department of Environmental Protection. Confirm permit history and compliance for any water‑adjacent improvements.

- Flood and elevation data. Verify FEMA flood zone, Base Flood Elevation, elevation certificates, and any history of flood claims.

You can independently check key records and context through official resources:

- Use the Miami‑Dade County Property Appraiser to review parcel data and tax history. Visit the property appraiser’s website via the Miami‑Dade portal for authoritative records.

- Verify recorded deeds and liens through the Miami‑Dade Clerk of the Courts records portal.

- Confirm FEMA flood zone designations and elevation references at the FEMA Flood Map Service Center.

- Review coastal and submerged lands permitting information at the Florida Department of Environmental Protection.

- For federal shoreline and dock permitting, consult the U.S. Army Corps of Engineers Jacksonville District’s permitting guidance.

Helpful links:

- Check FEMA flood maps and Base Flood Elevation at the FEMA Flood Map Service Center.

- Search parcel data at the Miami‑Dade County Property Appraiser.

- Review recorded documents at the Miami‑Dade Clerk of the Courts.

- Explore permitting guidance at the Florida Department of Environmental Protection.

- Review federal permit requirements at the U.S. Army Corps of Engineers Jacksonville District.

Model insurance before you commit

Obtain preliminary quotes for homeowners, wind, and flood coverage during your diligence period. Insurability and premiums are central to feasibility, and wind mitigation credits can materially change costs once documented. For current market context and consumer guidance, review resources from the Florida Office of Insurance Regulation, then have your broker shop both NFIP and private flood options.

- Learn more about insurance market conditions at the Florida Office of Insurance Regulation.

Prepare for a secure, on‑time closing

Most closings run through a Florida title company or escrow agent. Remote closings are possible, but plan for notarizations, corporate resolutions for entities, and time zone coordination if you are overseas. Schedule a final walk‑through to confirm condition, systems training, and a handover of gate credentials and dock access.

Immediately after closing, transfer utilities, update security systems and access lists, and set property management in motion. High‑value estates benefit from a dedicated manager who coordinates contractors, housekeeping, landscaping, and seasonal maintenance.

A streamlined timeline you can follow

- Pre‑offer, days to weeks

- Engage your broker and counsel. Sign NDAs as requested and submit proof of funds.

- Pre‑clear access with island security for any showings.

- Start insurance and lender conversations to understand feasibility.

- Offer and contract, days

- Finalize entity structure and funding sources.

- Submit an offer with concise contingencies and appropriate earnest money.

- Due diligence, typically 2 to 4 weeks

- Order title, survey, inspections, elevation certificates, and marine assessments.

- Confirm permits for any seawall, dock, or shoreline work.

- Secure insurance binders and finalize financing if applicable.

- Closing preparation, 1 to 3 weeks

- Clear title exceptions, coordinate wires, and schedule closing logistics.

- Arrange final walk‑through and access for the closing team.

- Post‑closing

- Transfer utilities, update gate access, and onboard property management and security.

- Confirm boat lift transfers and mooring rules if a dock is included.

Avoid common pitfalls

- Opaque pricing due to limited comparables. Use private sale intelligence and, if financing, expect specialized appraisals.

- Insurance surprises. Lock firm quotes for wind and flood coverage before you waive contingencies.

- Seawall or dredging liabilities. Always include a marine structural review and permit history check.

- Wire fraud risk. Confirm wiring instructions by phone with your known title contact. Do not act on unexpected emailed changes.

- Club membership assumptions. Membership policies can vary by property. Verify transfer rules, initiation fees, and any board approvals directly.

Buying on Indian Creek rewards preparation, discretion, and speed. With the right team, airtight documentation, and a tailored offer, you can move confidently in a market that prizes privacy and certainty. If you would like a quiet conversation about strategy, off‑market sourcing, and next steps, connect with Marine Luxury Waterfront. Schedule a private consultation with Marine Rollins.

FAQs

What makes buying on Indian Creek different?

- Inventory is minimal, many sales are off‑market, and showings are tightly controlled with NDAs and security clearance. Readiness and discretion often matter more than open competition.

How do showings work on Indian Creek Island?

- Your broker coordinates access with island security and the owner or manager. Expect to provide IDs, sign NDAs, and follow limits on photography or recording.

Can you finance an Indian Creek purchase?

- Yes, but jumbo lenders underwrite coastal properties more strictly with specialized appraisals and reserve requirements. Start lender conversations early to save time.

Which inspections are essential for a waterfront estate?

- Title and survey, whole‑home inspection, marine structural review of seawalls and docks, flood and elevation checks, and verification of permit history for shoreline work.

How do I verify flood risk and elevation?

- Use an elevation certificate and check FEMA flood zone and Base Flood Elevation at the FEMA Flood Map Service Center, then confirm with your surveyor and insurer.

Do properties include club membership automatically?

- Not necessarily. Membership terms, transferability, and approvals can vary by property. Confirm details directly before you commit.

How long does a typical closing take?

- With a prepared team, many luxury transactions move from contract to close in roughly 3 to 6 weeks, depending on due diligence, insurance, and entity documentation.

How can I keep my identity private when buying?

- Purchase through an LLC or trust arranged by counsel, route communications through your broker and attorney, and expect KYC and source‑of‑funds checks with banks and title.